{kind=link}

Introduction: The Cost of Idle Capital

Whether you have recently acquired a significant windfall—such as an inheritance, a business sale, or a lottery win—or have simply reached a level of professional success that leaves you with surplus liquidity, the worst financial decision you can make is to let that capital sit idle.

Traditional checking accounts are essentially “wealth-eroding” vehicles. When you account for the rate of inflation, a standard bank account effectively “shrinks” your purchasing power every year. To combat this, investors must choose a vehicle that balances their need for liquidity with their desire for growth. This guide provides a forensic comparison of the two most accessible and popular investment pillars: High-Yield Savings Accounts (HYSA) and Stocks/Exchange-Traded Funds (ETFs).

1. High-Yield Savings Accounts (HYSA): The Fortress of Liquidity

Think of a High-Yield Savings Account as a modernized version of the traditional savings account, engineered for the digital age. These accounts are primarily offered by online-only financial institutions that leverage lower overhead costs—such as the absence of physical branches—to pass higher interest rates back to the consumer.

The Advantages of the HYSA Model

- Principal Security: The primary appeal of an HYSA is that your initial investment is protected from market volatility. You do not wake up to find your balance has dropped by 20% due to a geopolitical event. In the U.S., these are typically backed by the FDIC, and in other regions, by equivalent government guarantees (like the FSCS in the UK or FCS in Australia), protecting balances up to specific limits (e.g., $250,000 per depositor).

- Immediate Liquidity: An HYSA acts as your financial “emergency brake.” Capital is highly liquid; you can typically transfer funds to a checking account within 24 to 72 hours, making it the ideal home for an “Emergency Fund” or a “House Deposit Fund.”

- Ease of Management: Unlike the stock market, which requires a steep learning curve and constant monitoring, an HYSA is “set and forget.” It is an entry-level wealth-building tool that requires zero technical analysis.

The Disadvantages: The Invisible Thief

- Inflation Risk: While your balance grows in numerical terms, it may shrink in real terms. If an HYSA offers 4.5% interest while the Consumer Price Index (CPI) reflects 5% inflation, your “real” return is -0.5%.

- Interest Rate Fluctuations: These rates are variable. They are intrinsically tied to the central bank’s “prime rate.” When the Federal Reserve or similar bodies lower interest rates to stimulate the economy, your HYSA yield will likely drop accordingly.

:max_bytes(150000):strip_icc():format(webp)/how-interest-rates-work-savings-accounts.asp-3644536378554b9ab3ecab2747aa066c.jpg)

2. Stocks and ETFs: The Engine of Exponential Wealth

Investing in the stock market represents a transition from a “Saver” to a “Part-Owner.” When you purchase shares in an individual company or an Exchange-Traded Fund (ETF)—which is essentially a basket of hundreds or thousands of companies, such as those in the S&P 500—you are betting on the long-term productivity of the global economy.

The Advantages of Equity Participation

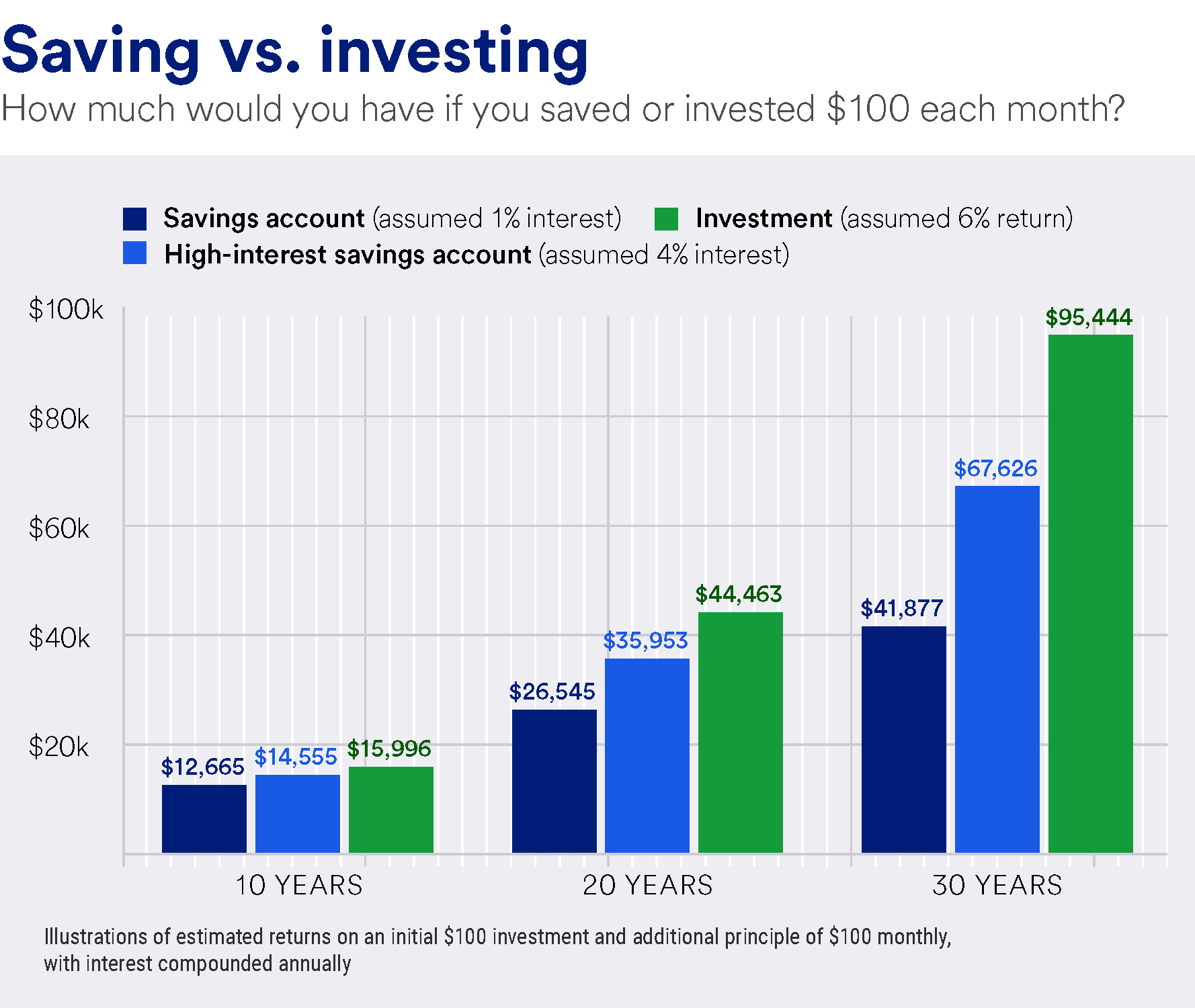

- Superior Historical Growth: Historically, the S&P 500 has returned an average annual rate of approximately 7% to 10% after inflation. Over a 20-year horizon, this creates a compounding effect that HYSAs simply cannot match.

- Dividend Income: Many mature companies pay out a portion of their profits to shareholders. These dividends can be taken as cash (passive income) or, more strategically, reinvested through a DRIP (Dividend Reinvestment Plan) to buy more shares, accelerating the snowball effect of wealth.

- Diversification via ETFs: ETFs allow an investor to own a slice of the entire market. This “baskets of stocks” approach mitigates the risk of a single company failing, as the success of the remaining companies in the index buffers the loss.

The Disadvantages: The Emotional Toll

- Market Volatility: The stock market is prone to “Recessions” and “Corrections.” It is psychologically taxing to see a portfolio drop by tens of thousands of dollars in a single week. Success in this field requires “Iron Stomach” discipline—the ability to hold through the storm rather than panic-selling.

- Complexity and Tax Implications: Selling stocks for a profit triggers Capital Gains Tax, which requires meticulous record-keeping and a more complex tax filing process compared to simple interest income.

. The “Bucket Method” Strategy: A Time-Horizon Framework

Professional financial advisors rarely suggest choosing only one. Instead, they recommend the “Bucket Method,” which aligns your investment choice with your specific time horizon.

Bucket 1: The Short-Term (0–3 Years)

Vehicle: High-Yield Savings Account. Purpose: Saving for a wedding, a down payment, or an emergency fund. You cannot risk these funds in the market because a downturn the month before your wedding would be catastrophic.

Bucket 2: The Medium-Term (3–7 Years)

Vehicle: A 50/50 Balanced Split. Purpose: Major lifestyle upgrades or early retirement planning. This balanced approach uses the HYSA interest to “buffer” the potential volatility of the Stock/ETF portion.

Bucket 3: The Long-Term (7+ Years)

Vehicle: Aggressive Stock and ETF allocation. Purpose: Retirement or generational wealth. Over a 10-year period, the probability of the stock market being “up” is significantly higher than it being “down.”

4. Legal & Professional Analysis

Regulatory Safeguards

In the United States, HYSAs are regulated under Regulation DD (Truth in Savings Act), which requires banks to disclose APY (Annual Percentage Yield) clearly. Stocks and ETFs fall under the jurisdiction of the SEC (Securities and Exchange Commission), ensuring that public companies provide transparent financial reporting.

Tax Treatment

- HYSA Interest: This is generally taxed as “Ordinary Income” at your marginal tax rate. It is treated the same as the salary from your job.

- Stocks/ETFs: These are subject to Capital Gains Tax.

- Short-Term: (Held for less than a year) Taxed at ordinary income rates.

- Long-Term: (Held for over a year) Taxed at lower, preferential rates (0%, 15%, or 20% in the U.S.), making long-term stock holding more “tax-efficient” than a savings account.

FAQ: Frequently Asked Questions

Q: Can I lose money in a High-Yield Savings Account? A: Virtually never, as long as the bank is FDIC/government-insured and you are within the coverage limits. The only “loss” is the opportunity cost and the potential loss of purchasing power if inflation exceeds your interest rate.

Q: Is it “gambling” to invest in the S&P 500? A: No. Gambling is a zero-sum game with a house edge. Investing in a broad-market ETF is a bet on the continued growth and innovation of the world’s largest companies. Historically, the “house” (the market) has always gone up over the long term.

Q: How much should I keep in my “Emergency Fund” bucket? A: Most experts recommend 3 to 6 months of essential living expenses. This money should stay in an HYSA where it is instantly accessible, regardless of what the stock market is doing.

Q: What is the best ETF for a beginner? A: Low-cost index funds that track the total market (like VTI) or the S&P 500 (like VOO or SPY) are widely considered the gold standard for beginning investors due to their low fees and high diversification.

Conclusion: The Wealth Creator’s Mindset

Choosing between an HYSA and the Stock Market is not an “either-or” decision; it is a “when” decision. A professionally managed portfolio utilizes the HYSA as a defensive shield and the Stock Market as an offensive sword. By implementing the Bucket Method, you ensure that you are protected against today’s emergencies while being positioned to harvest the rewards of tomorrow’s growth.

Legal Disclaimer: The information provided in this article is for educational and analytical purposes only and does not constitute financial, legal, or investment advice. Investing involves risk, including the possible loss of principal. Always consult with a certified financial planner or tax professional before making significant allocation decisions.