When examining global personal finance, a stark paradox emerges between escalating macroeconomic indicators—such as soaring stock market valuations and expanding global Gross Domestic Product (GDP)—and the microeconomic reality experienced by the average individual. To understand the true state of global financial resilience, we must look past the misleading nature of top-line averages and examine the absolute liquidity floor: the number of individuals who lack even a basic financial buffer.

Click here to receive $1000 in cash

As we cross into mid-2026, compiling financial metrics from major institutions like the Credit Suisse/UBS Global Wealth Report, the World Bank Findex Database, and global consumer research firms reveals a profound lack of liquid emergency reserves worldwide.

🌎 The Liquidity Floor: How Many Adults Have Less Than $1,000?

Quantifying exactly how many adults worldwide possess less than $1,000 in liquid savings requires drawing a clear line between net worth (which includes illiquid assets like real estate, agricultural land, and retirement pensions) and liquid cash savings (instantly accessible capital held in bank accounts, digital wallets, or physical cash).

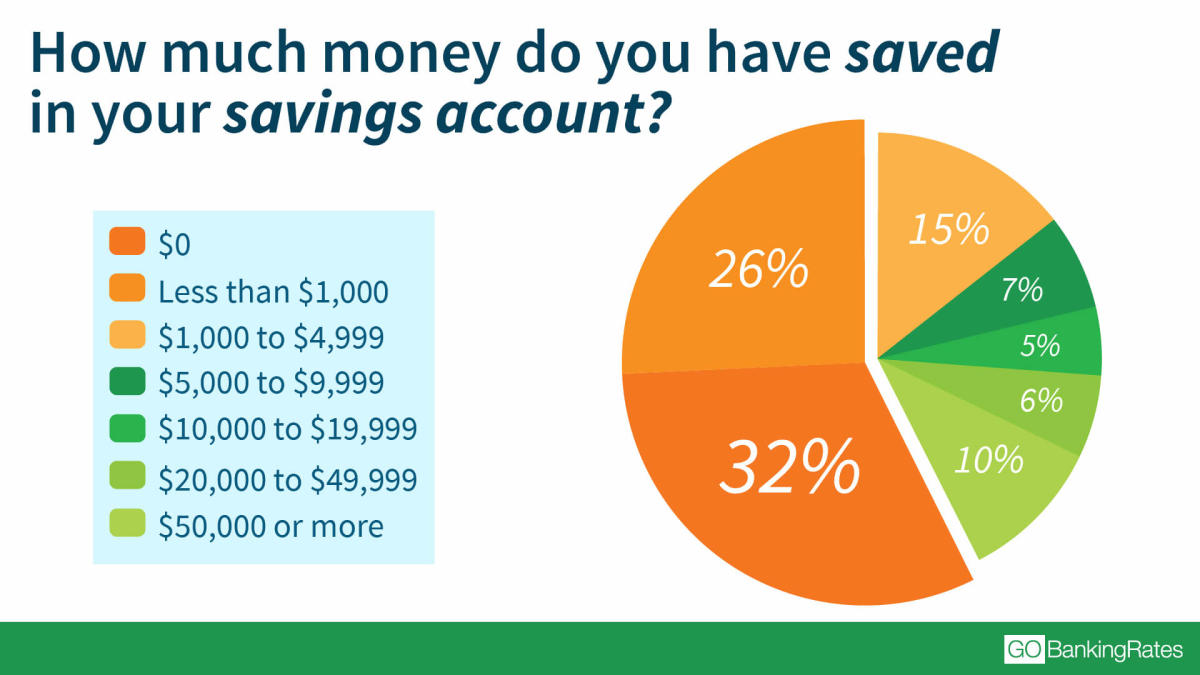

On a global scale, the adult population sits at approximately 5.5 billion individuals. Strikingly, comprehensive analysis of global banking access and deposit distributions indicates that approximately 55% to 60% of all adults worldwide possess less than the equivalent of $1,000 USD in liquid cash savings. This amounts to an estimated 3.0 billion to 3.3 billion people living without a functional financial safety net.

This systemic lack of cash reserves is not distributed evenly, and it splits cleanly across two distinct economic realities:

1. Developing and Emerging Economies

In low-to-middle-income nations across Sub-Saharan Africa, South Asia, and parts of Latin America, the primary barrier to liquid accumulation is low baseline income and a high rate of unbanked populations. According to World Bank data, while mobile money accounts (such as M-Pesa or bKash) have drastically increased financial inclusion, the vast majority of these accounts are utilized for transactional velocity—immediately paying for food, utilities, and fuel—rather than capital accumulation. For billions of adults in these regions, saving $1,000 USD is an impossibility when the median daily wage remains below $5 to $10 USD.

{kind=link}

2. Advanced and High-Income Economies

More surprisingly, a significant percentage of this 3-billion-person cohort resides within affluent nations like the United States, the United Kingdom, and parts of Western Europe.

In the United States, Federal Reserve consumer surveys consistently show that roughly 35% to 40% of adults cannot comfortably cover a $400 unexpected emergency expense using cash or its equivalent. In the UK and Australia, persistent inflationary pressures on housing, energy, and groceries over the last few years have thoroughly eroded middle-class discretionary margins. In these high-income environments, the phenomenon is driven by structural “lifestyle inflation,” high debt-to-income ratios, and skyrocketing rental or mortgage obligations, trapping millions in a cycle of living paycheck to paycheck despite earning historically high nominal wages.

This persistent cash deficit highlights a much deeper systemic issue: the institutionalization of living paycheck to paycheck across the modern workforce. Even as nominal earnings rise, the compounding pressures of lifestyle inflation and rising debt structures trap millions in a continuous loop of financial anxiety. To explore the exact psychological and macroeconomic mechanisms that fuel this dynamic—and to access actionable steps to break the loop—read our full breakdown on The Global Paycheck Crisis: Understanding and Overcoming the Financial Cycle.

Global Savings Benchmarks: Median vs. Mean

To fully appreciate why so many adults remain cash-poor despite staggering global wealth generation, we must understand the mathematical divergence between the mean (average) and the median (the absolute middle point) of global wealth.

[Total Global Adult Population: ~5.5 Billion]

├── Top 1% to 10% (Concentrated Trillions in Assets/Equities) --> Skews MEAN Upward

├── Exact Center Individual (Median Cash Balance) --> Represents MEDIAN (~$1,200)

└── Lowest 55-60% (Under $1,000 in Liquid Savings)

In wealth distribution analysis, the mean is a highly distorted metric. If an ultra-high-net-worth individual with $50 billion enters a room of 10,000 bankrupt individuals, the mean net worth of the room instantly jumps to $5 million per person. However, the median remains exactly $0.

The Global Mean (Average) Net Worth

According to the latest aggregated global wealth data, the average net worth per adult worldwide hovers around $85,000 to $90,000 USD. On paper, this implies a highly resilient global populace. However, this figure is heavily skewed upward by the top 1% to 10% of global citizens who hold vast portfolios of equities, real estate, and corporate ownership. It completely masks the structural fragility of the remaining 90%.

The Global Median Net Worth

When we shift our lens to the true middle point of humanity—where 50% of adults sit above and 50% sit below—the global median net worth plummets to approximately $8,500 to $9,000 USD.

The Ultimate Reality: Liquid Cash Median

When you peel back the illiquid components of that median net worth (such as a tiny plot of ancestral land, a depreciating vehicle, or a heavily mortgaged apartment) and isolate pure liquid savings, the global median cash balance drops to an estimated $1,200 USD. This means that if you have more than $1,200 in a liquid bank account right now, you are financially healthier than half of the human beings on Earth.

Structural Causes of the Global Liquidity Deficit

Several compounding macroeconomic shifts have institutionalized this global lack of savings:

-

Negative Real Interest Rates vs. Core Inflation: For several years, while banks offered near-zero interest on standard transaction accounts, the real-world cost of living (food, shelter, insurance) escalated at a rapid pace. This meant savers were effectively penalized, as the purchasing power of their cash eroded faster than the nominal interest could compound.

-

The Financialization of Assets: In modern economics, surplus capital is rarely left to sit in liquid cash. Wealthy individuals immediately funnel excess capital into yield-generating assets (stocks, ETFs, private equity, property). Conversely, lower-income individuals do not have access to these wealth-compounding vehicles, widening the gap between the asset-owning class and the cash-strapped working class.

-

The Gig Economy and Income Volatility: The global rise of independent contracting, gig work, and casualized labor has replaced predictable, salaried income with highly volatile revenue streams. Without a predictable baseline income, structural budgeting and long-term automated savings habits become vastly more difficult to maintain.

❓ Frequently Asked Questions

Q1: Why do global reports show high wealth metrics while individual savings are so low?

Most prestigious wealth reports (like those from UBS or the World Bank) measure total wealth, which includes real estate equity, pension funds, and business assets. While an individual might own a home worth $500,000, they may simultaneously have less than $500 in their liquid checking account due to high mortgage payments and living expenses. This is known as being “asset-rich but cash-poor.”

Q2: What country has the highest median savings per adult?

Historically, countries like Switzerland, Australia, and Hong Kong consistently trade the top positions for the highest median wealth per adult. Australia, for instance, benefits heavily from a mandatory, universal retirement savings system (Superannuation) and high rates of property ownership, which dramatically lifts the median wealth baseline compared to nations with lower systemic social safety nets.

Q3: How much liquid savings should an adult ideally hold?

Financial planners universally recommend maintaining an emergency fund containing 3 to 6 months of essential living expenses kept in a highly liquid, accessible vehicle like a High-Interest Savings Account (HISA). This capital should be insulated from market volatility and reserved strictly for unexpected medical events, job losses, or urgent structural repairs.